How we created our advised portfolios

When we set out to build advised portfolios, our goal was simple: create diverse, low-fee, tax-efficient portfolios. Here’s a look at the thinking behind how we made them.

With advised portfolios, we focused on some of the key concepts that shape every portfolio: risk and return, diversification, asset classes, and managing currency risk—let’s look at each.

Risk and return

All investing involves a trade-off between risk and expected return.

Risk isn’t just about ups and downs in price—it’s the possibility of losing some or all of your money. Investments with higher potential returns tend to come with a greater chance of loss. Those that are more stable tend to offer lower returns over time.

Why is this? Riskier investments tend to offer higher expected returns to attract investors, as they generally require compensation for taking on additional uncertainty.

Different investors need different trade-offs. Someone saving for a house deposit in two years has different needs than someone investing for retirement in thirty years. The question is: how much uncertainty are you comfortable with, and for how long?

It's worth noting that taking on too little risk can also work against you. If your investments are too conservative for your timeframe, you may miss out on the returns you need to meet your long-term goals.

The right portfolio for you depends on your timeframe, your comfort with ups and downs, and your financial situation. When you go through our advice flow, we ask about these factors to match you with a suitable portfolio—whether that's conservative, balanced, growth, or high-growth.

Diversification

To meet your investment goals, you'll need a certain level of expected returns. But here's the question: can you target those returns while avoiding unnecessary risk?

This is where diversification comes in. If all your money is in a single investment and it falls, your whole portfolio falls with it. But if you spread across multiple investments that don't all move together, a drop in one has less impact. Others may hold steady or even rise, cushioning the blow.

The key insight is that diversification can reduce risk without necessarily reducing expected returns. By combining investments that behave independently, the ups and downs partially offset each other.

You're not necessarily giving up growth potential—you're smoothing out the ride.

But not all combinations are equally effective. Some investments are closely linked—if one drops, the other tends to drop too. The most effective diversification comes from combining investments that genuinely behave differently.

Asset classes

An asset class is a way of grouping investments that tend to behave similarly.

Asset classes are a standard concept in the investment industry—you'll see them disclosed in the product disclosure statements of most investment funds—and are sometimes referred to as an 'investment mix'.

Different providers may group them slightly differently, but the core idea is the same.

Asset classes help us do two things:

Position funds on the risk-return spectrum—different asset classes offer different levels of risk and expected return.

Diversify effectively—different asset classes respond differently to market conditions, so combining them reduces overall volatility.

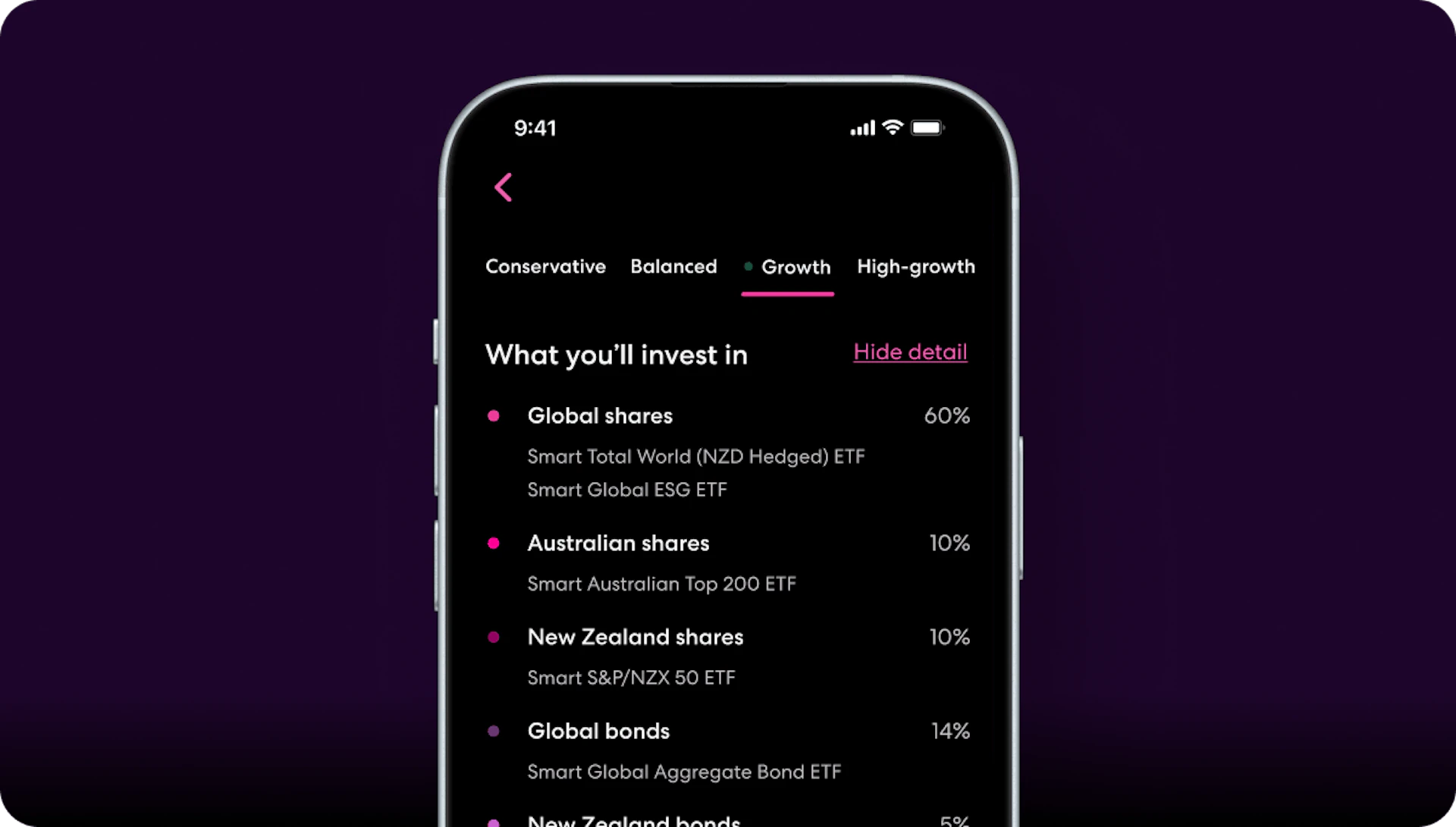

Our portfolios are made up of five main asset classes:

Cash—the most stable: lowest risk, lowest return.

NZ fixed income (bonds)—lending to New Zealand companies and government.

International fixed income (bonds)—lending to overseas companies and governments.

NZ and Australian equities (shares)—owning a piece of local and regional companies.

International equities (shares)—owning a piece of companies around the world.

Why bonds and shares behave differently

The most important distinction is between debt (bonds) and equity (shares).

When you invest in a bond, you're essentially lending money to a company or government. Like a bank loan, the terms are agreed upfront—the bondholder receives a set amount over a set period. Bondholders sit near the front of the queue if things go wrong.

If a company runs into trouble and needs to pay back its debts, bondholders generally get paid before shareholders see anything.

That security comes with a trade-off: bondholders don't share in the company's success. If the company has a record year, your bond still pays the same agreed return.

Shares work differently. When you buy shares, you own a piece of the company. There's no guaranteed repayment—if the company struggles, your investment can lose value, and shareholders are generally last in line if the company fails. But if the company grows and thrives, shareholders participate in that success. That's why shares have historically offered higher returns over the long term, but with more ups and downs along the way.

Because bonds and shares are structured so differently, they tend to respond differently to economic conditions. When share markets fall, bonds often hold their value or even rise as investors seek stability.

This makes them effective diversifiers when combined.

Why we invest across different countries

We also split our investments across local and international markets.

Companies within the same country share exposure to many of the same forces: a domestic recession, a change in interest rates, or new tax policy will affect most businesses in that market. Companies in other countries face different conditions, which is why geographic diversification works—you're not fully exposed to what happens in any single economy.

Investing across multiple countries also gives you access to a broader set of opportunities. Local markets like New Zealand represent a small fraction of global economic activity, so looking beyond our borders opens up significantly more possibilities.

Diversifying within asset classes

Diversifying across asset classes is important, but it's not enough on its own. If you held just one share and one company bond, you'd still be exposed to the fortunes of those two individual companies. True diversification means spreading your investments within each asset class as well.

This is where exchange-traded funds (ETFs) and managed funds come in. Rather than buying individual shares or bonds, these funds pool money to invest in dozens or even thousands of companies at once. A single international shares fund might hold positions in thousands of companies across multiple countries and industries—from technology to manufacturing to financial services. This means you get broad exposure to an entire asset class without being reliant on any single company's performance.

By using ETFs and managed funds in our portfolios, our aim is to ensure you're diversified both across and within asset classes.

Managing currency risk

When you invest internationally, your return in New Zealand dollars has two parts: the return in the investment's local currency, and the effect of exchange rate movements.

All investments held in the same foreign currency share that currency component. This can cause otherwise independent investments to move together, reducing the effectiveness of diversification.

Currency hedging removes the currency component. This means your returns better reflect the underlying investments, which behave more independently—exactly what we want for effective diversification.

International bonds

For bonds, the currency component is particularly problematic.

Bond returns are modest, so currency movements can easily dominate—adding volatility to an asset meant to provide stability.

Hedging removes the currency component, reducing volatility and improving diversification.

However, hedging isn't free—the cost effectively converts the foreign return into something similar to what you'd get from New Zealand bonds.

So why include international bonds at all? The benefit isn't higher returns—it's diversification across different issuers and credit markets, while maintaining bond-like stability. We fully hedge our international bonds to preserve their stabilising role in the portfolio.

International equities

For equities, currency movements make up a smaller proportion of total return, so the impact is less pronounced. Some currency exposure can even provide a benefit. For example, if the New Zealand economy underperforms and the NZD falls, your unhedged international investments are worth more in NZD terms. However, the reverse is also true: if the NZD rises, unhedged investments are worth less. We take a balanced approach for international equities, hedging a portion of the currency exposure while retaining some. This reduces the correlation introduced by currency movements, while keeping some foreign currency exposure as a buffer.

Currency hedging comes at a cost, so there's a balance to strike—we aim to manage currency risk without over-hedging.

Making it yours

Everything we've covered—diversification, asset classes, currency hedging—is built into each of our portfolios. Once you're matched with a portfolio, you can tailor it further by adjusting the mix of passively and actively managed funds, and choosing whether to include environmental, social, and governance (ESG) screened funds.

Passively managed funds

Our portfolios can include both passively and actively managed funds.

Passively managed funds aim to track a market index, and hold assets roughly in proportion to the value the market has determined. For example, an international shares index represents the value of companies across global markets: a passive fund tracking it will hold those companies in similar proportions. There's no fund manager deciding what to buy or sell—the fund simply reflects the market as a whole.

Actively managed funds

Actively managed funds are different. Fund managers research companies, analyse markets, and make decisions about what to buy, hold, or sell—essentially betting that they can identify opportunities the market has mispriced. This takes time and expertise, which means higher costs. These costs are passed on to investors through higher management fees.

Historically, most actively managed funds have struggled to consistently outperform the market after fees are taken into account.

However, whether actively managed funds can add value remains an ongoing debate—some investors believe skilled managers can identify opportunities that passive funds miss.

Passively vs actively managed funds

Our portfolios default to passively managed funds, keeping management fees lower. If you'd prefer, you can adjust your portfolio to include actively managed funds—but keep in mind that this is the main driver of management fees in your portfolio.

You don't have to choose all of one or the other. Our portfolios let you adjust the balance between passively and actively managed funds. If you're unsure whether actively managed funds can add value, you can take a balanced approach by allocating a portion to actively managed funds while keeping the rest passive. This can help manage your fee exposure while leaving room for active managers to add value if they can. You’ll be able to see in your advised portfolio how each fund is performing over time.

ESG and ethical investing

You can tilt your portfolio towards ethically focused funds if you want your investments to better reflect your values.

Environmental, social, and governance (ESG) criteria used to screen investments is based on factors like carbon emissions, labour practices, and corporate ethics. ESG funds typically exclude or underweight companies that don't meet certain standards, and may favour those with stronger ESG practices.

It's worth noting that ESG screening isn't perfect. Different providers use different methodologies, and much of the data relies on company disclosures. An ESG label doesn't guarantee a company is fully aligned with your values, but it does reflect an effort to incorporate these considerations into investment decisions.

ESG fund options are still limited in the market, so we've had to blend ESG and non-ESG funds to maintain proper diversification and currency management. As more ESG funds become available, we'll look to increase coverage.

Wrapping up

From understanding risk and return, to diversification, asset classes, and currency management—every decision supports one goal: providing you with a diverse, low-fee, tax-efficient portfolio that fit your goals, your timeline, financial security, and comfort with risk.

Get an advised portfolio in minutes

Advised portfolios are a smart way to create a diversified investment portfolio that’s tailored to you and your values—without needing to pick the underlying investments.

Investing involves risk. You might lose the money you start with. See our advised portfolio page for information on advised portfolios. Sharesies Limited holds a Financial Advice Provider (FAP) licence issued by the Financial Markets Authority (FMA). See our advice disclosure statement.

Join over 1,000,000 investors