How we rebalance your advised portfolio

Investing isn’t just about choosing the right mix of investments—it’s about keeping that mix aligned with your goals over time. With our advised portfolios, we aim to do both.

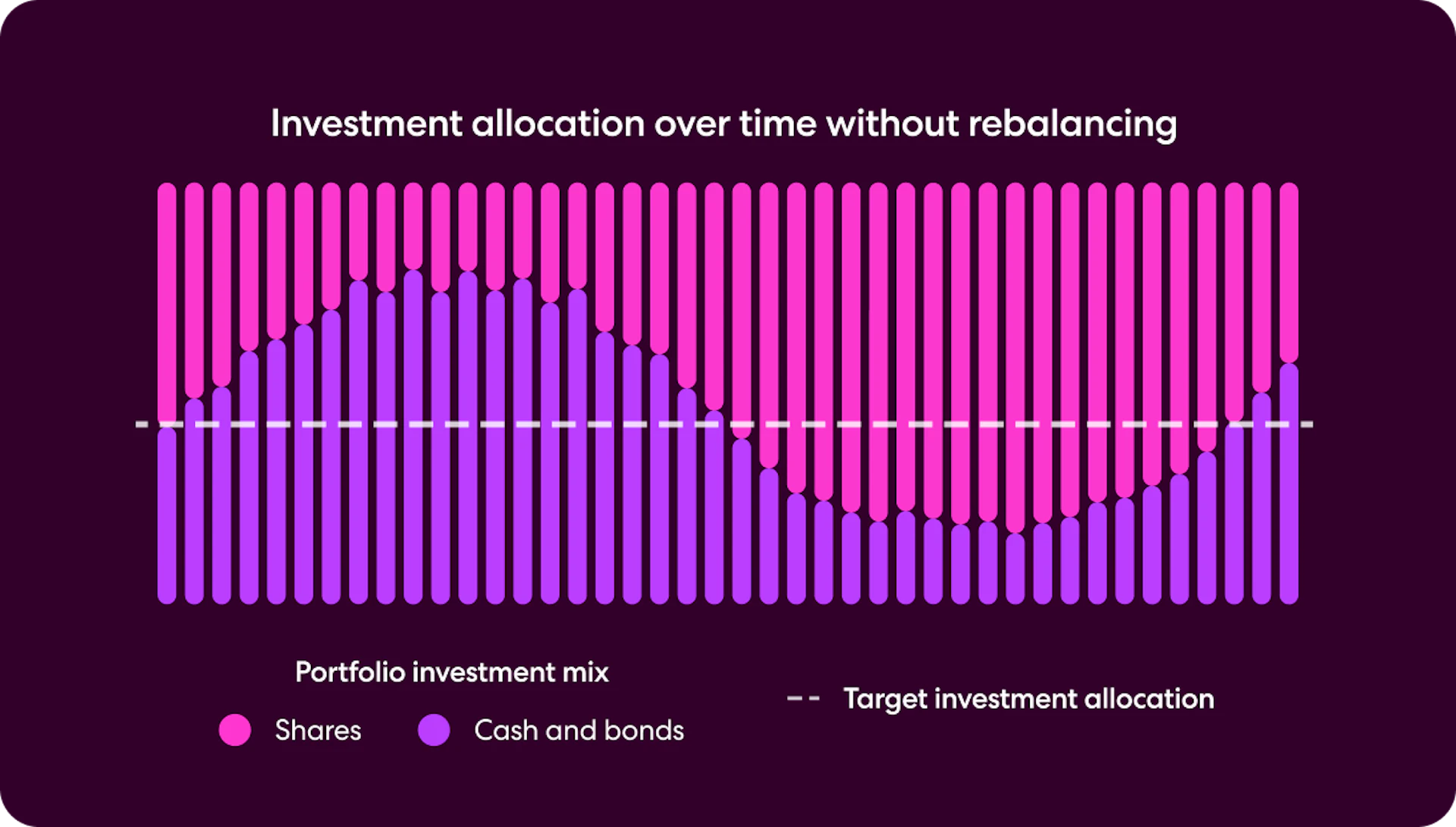

As markets move and investments change value at different rates, a portfolio can slowly drift towards an unintended risk level—for example, from balanced to growth.

To manage this drift in our advised portfolios, we rebalance them. It’s a thoughtful, research-backed process designed to keep an investment on track, reduce unnecessary risk, and support better long-term outcomes.

Why portfolios drift over time

Every investment behaves differently. Over the long term, shares are generally expected to outperform bonds, but bonds generally provide more stability during market downturns. Because of this difference, the allocation between investments in a portfolio naturally drifts.

How portfolio drift works

When markets are strong—shares often grow faster than other investments, increasing their allocation within the portfolio. A growth portfolio could unintentionally drift toward a high growth portfolio.

When markets are weak—shares may fall in value relative to other investments, reducing their allocation within the portfolio. A growth portfolio could unintentionally drift toward a balanced portfolio.

Left unchecked, this drift can quietly shift a portfolio away from its intended risk level.

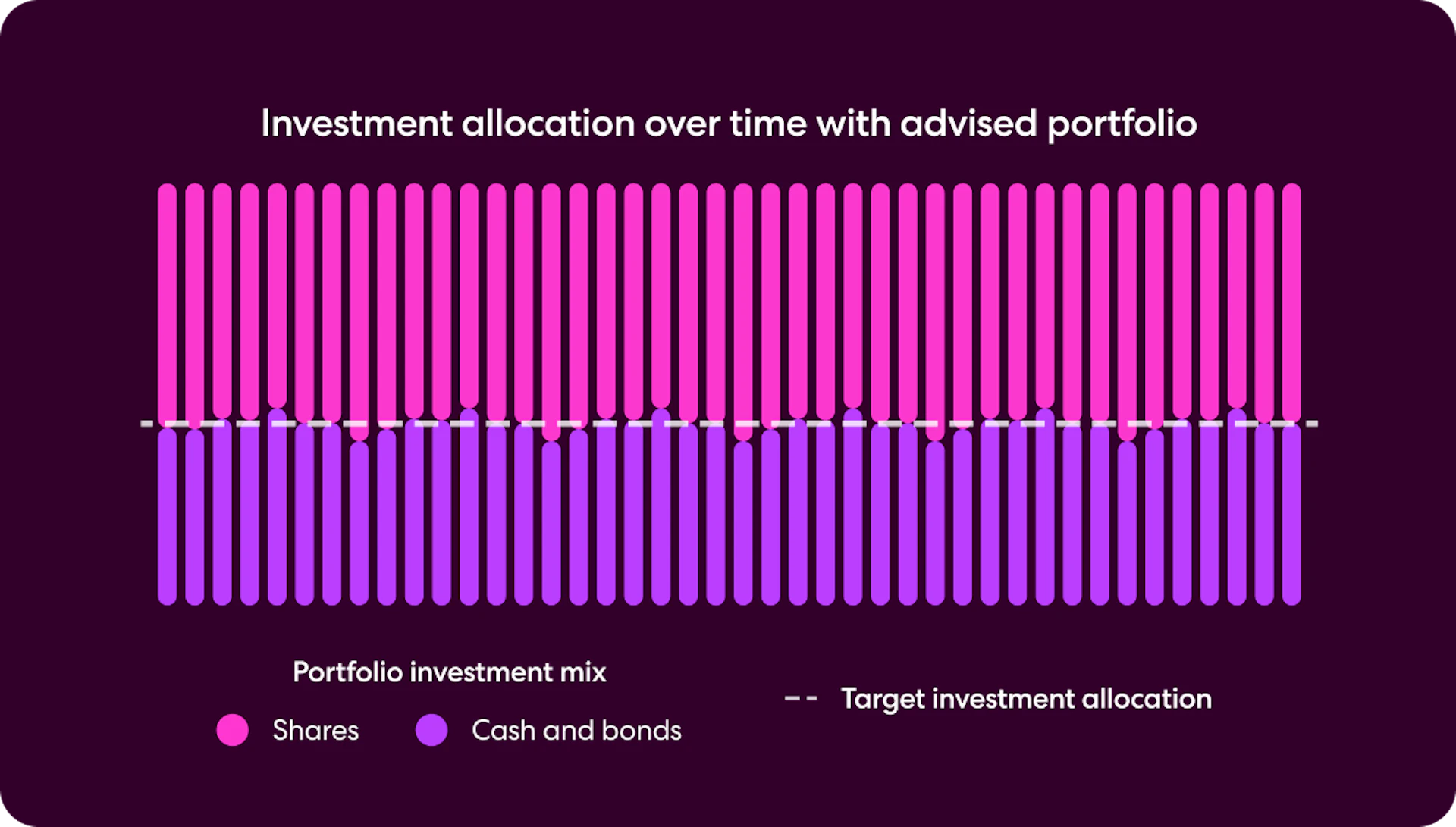

Rebalancing keeps your portfolio on track

To maintain consistent risk levels, we gently nudge your portfolio back towards its target allocation.

Rebalancing works by:

buying the investments that have fallen below their target weighting

selling the ones that have grown above their target weighting.

This helps keep your portfolio aligned with your chosen mix of growth and defensive investments.

For example

Let’s say you invest $10,000 into a portfolio with a target allocation of 60% shares and 40% bonds.

The initial allocation would be:

$6,000 shares (60% of the total portfolio value)

$4,000 bonds (40% of the total portfolio value)

Over time, imagine the shares grow by 10% and the bonds grow by 4%—they would now be worth:

shares: $6,600 (~61.3% of the total portfolio value)

bonds: $4,160 (~38.7% of the total portfolio value)

The difference in investment performance has resulted in this portfolio drifting away from its target allocation.

To rebalance the portfolio, we would sell some shares and buy more bonds. This would bring the allocation back to 60% shares and 40% bonds, and keep the portfolio aligned with its intended risk level.

The rebalancing trade-off

How often should a portfolio be rebalanced? There’s a trade-off to consider:

Rebalancing more frequently—keeps your portfolio more tightly aligned with its target allocation, but typically comes with more transaction costs (which can erode returns).

Rebalancing less frequently—reduces transaction costs, but allows your portfolio to drift further from its target allocation.

Research from Vanguard found that annual rebalancing with a 1–2% drift threshold balances these trade-offs well—which we confirmed with our own analysis of the funds in our portfolios.

There are diminishing returns to rebalancing more frequently than annually, as it only provides small improvements in tracking accuracy. That said, when transaction costs are minimised or removed (as they are with advised portfolios), more frequent rebalancing becomes attractive because you get tighter alignment without the cost.

How we rebalance your advised portfolio

Your advised portfolio is automatically rebalanced once every quarter, as well as when you buy or sell. We don’t charge any additional transaction fees when we rebalance it.

Quarterly rebalancing

Every quarter, we review your advised portfolio and rebalance it back to its target allocation.

We don’t charge transaction fees when we rebalance, which makes more frequent rebalancing worthwhile. (Transaction costs charged by the underlying fund managers still apply.) This keeps your advised portfolio closely aligned with your intended risk level.

Rebalancing when you buy or sell

Whenever you add money to your advised portfolio—or withdraw from it—we use that moment to adjust the mix of investments back toward the target allocation. This helps reduce drift naturally without additional trading.

What rebalancing doesn’t do

Rebalancing is a risk management tool, not a strategy to increase returns. It won't protect your portfolio from overall market downturns. For example, if shares and bonds fall together, your portfolio value will still decline.

Over the long run, rebalancing may even slightly reduce returns compared to a portfolio that’s not rebalanced, as it often involves reducing the allocation to growth investments. If you're seeking higher returns over a long timeframe, you might consider whether a higher-risk portfolio better suits your goals—and not rely on portfolio drift to get you there.

Finally, rebalancing assumes your target allocation is still right for you. If your financial situation or goals change, it's worth reviewing whether your chosen portfolio still suits your needs. Additionally, you can create multiple advised portfolios that suit different goals and timeframes.

The best outcome for you

Rebalancing isn't about chasing returns. It's about making sure your portfolio stays true to the risk level you chose, through all market conditions. By keeping your investment mix on track, rebalancing helps ensure your investment experience remains consistent with your goals over the long term.

Get an advised portfolio in minutes

Advised portfolios are a smart way to create a diversified investment portfolio that’s tailored to you and your values—without needing to pick the underlying investments.

Now for the legal bit

Investing involves risk. You might lose the money you start with. See our advised portfolio page for information on advised portfolios. Sharesies Limited holds a Financial Advice Provider (FAP) licence issued by the Financial Markets Authority (FMA). See our advice disclosure statement.

Join over 1,000,000 investors